Double Materiality Unpacked: CSRD Insights and Practical Strategies for Businesses

How much of a social concern is viable for a company to demonstrate and be sustainable?

This question echoes through boardrooms as companies grapple with CSRD’s double materiality concept. It’s a balancing act, much like the interplay between Earth’s atmosphere and its life forms. A company’s actions ripple through both its financial ecosystem and the wider world, creating a complex web of cause and effect that extends far beyond the balance sheet.

Double materiality is CSRD’s way of saying, “It’s complicated.” On one side, we have financial materiality – how sustainability issues might fatten or slim a company’s wallet. On the flip side, there’s impact materiality – the company’s footprint on the world, be it a gentle pat or a heavy stomp.

CSRD isn’t asking companies to choose between profit and planet. Instead, it’s demanding they understand the intricate dance between the two. It’s like trying to manage an ecosystem while running a business – challenging, but crucial for long-term survival.

So, what exactly does CSRD expect? Let’s break it down:

- Comprehensive assessment: Dig deep, examining both your impacts on sustainability and how sustainability might impact your bottom line. No stone left unturned.

- Interconnected analysis: Don’t just list issues. Show how they intertwine, like a complex web of ecosystems. Your carbon emissions today might be your financial risk tomorrow.

- Value chain focus: Look beyond your four walls. Your supplier’s labor practices or your customer’s waste habits? They’re your problem now.

- Long-term view: Sustainability isn’t a quarterly report. Think in terms of years, decades even. What seems immaterial now might be crucial in 2050.

- Stakeholder engagement: No company is an island. Talk to your employees, customers, communities. Their concerns are your materiality issues.

Here’s the kicker: most companies are currently focusing on qualitative reporting of double materiality. It’s like trying to describe a complex ecosystem with words alone – you might capture the surface, but miss the intricate interactions beneath.

Addressing the interdependencies is where it gets really tricky. It’s like managing a complex ecosystem – each action ripples through the system, affecting multiple elements in often unexpected ways. A single business decision can cascade through both financial and impact domains, creating a ripple effect that’s hard to predict but crucial to understand.

To tackle this, companies might:

- Develop integrated frameworks: Merge sustainability and financial analyses. It’s not either/or, it’s both/and.

- Use scenario analysis: Explore potential futures. What if climate change accelerates? What if consumers demand 100% recyclable packaging?

- Form cross-functional teams: Bring together sustainability experts and financial analysts. Let them duke it out and find common ground.

- Adopt dynamic assessments: Materiality isn’t static. What’s immaterial today might be crucial tomorrow.

Using the report “Early Adopter’s CSRD Reporting – Inspiring reporting practice from reporting year 2023 from We Mean Business coalition, we have analysed the double materiality representation of different companies in their CSRD reports

Source: Early Adopter’s CSRD Reporting – Inspiring reporting practice from reporting year 2023

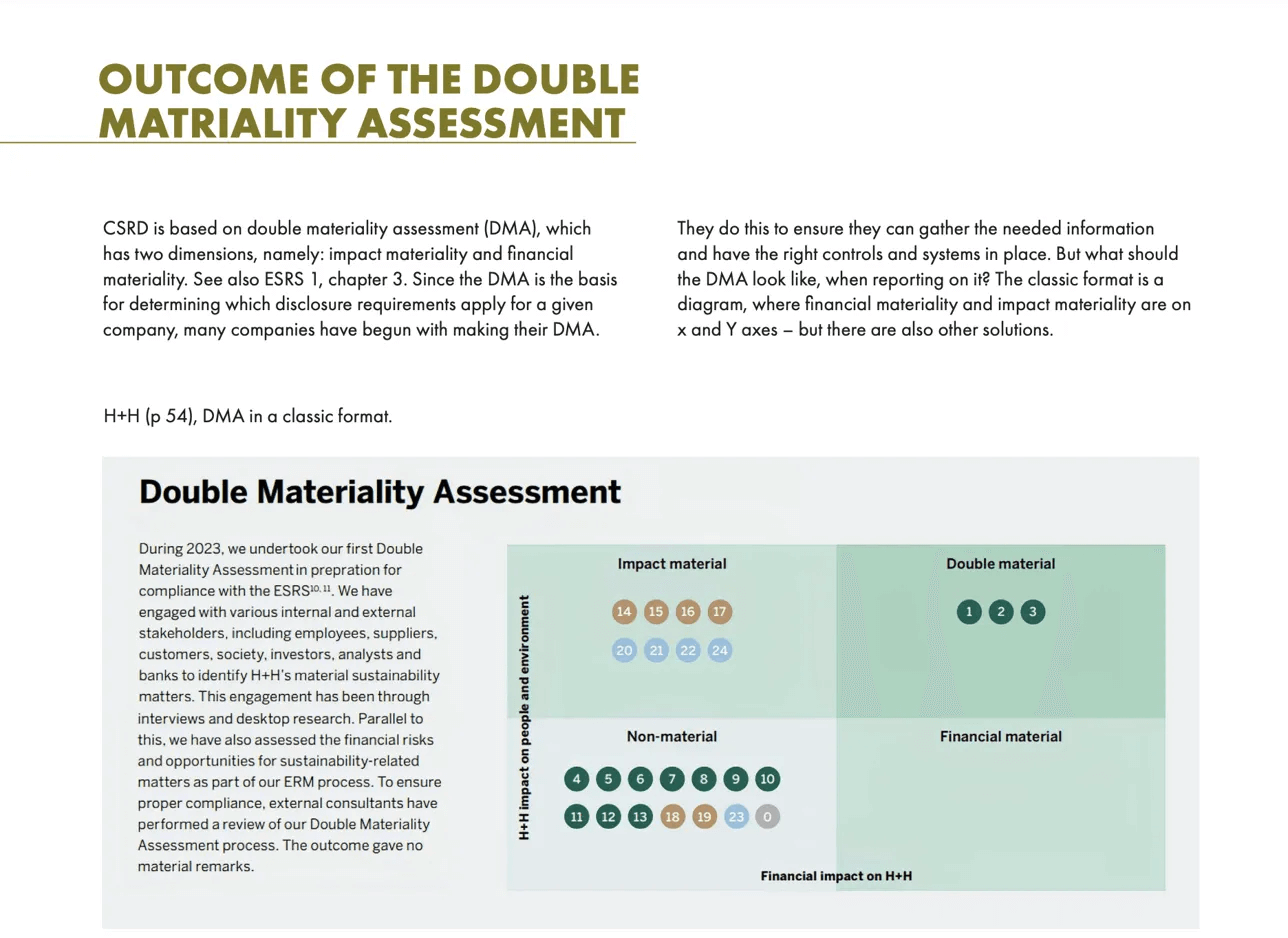

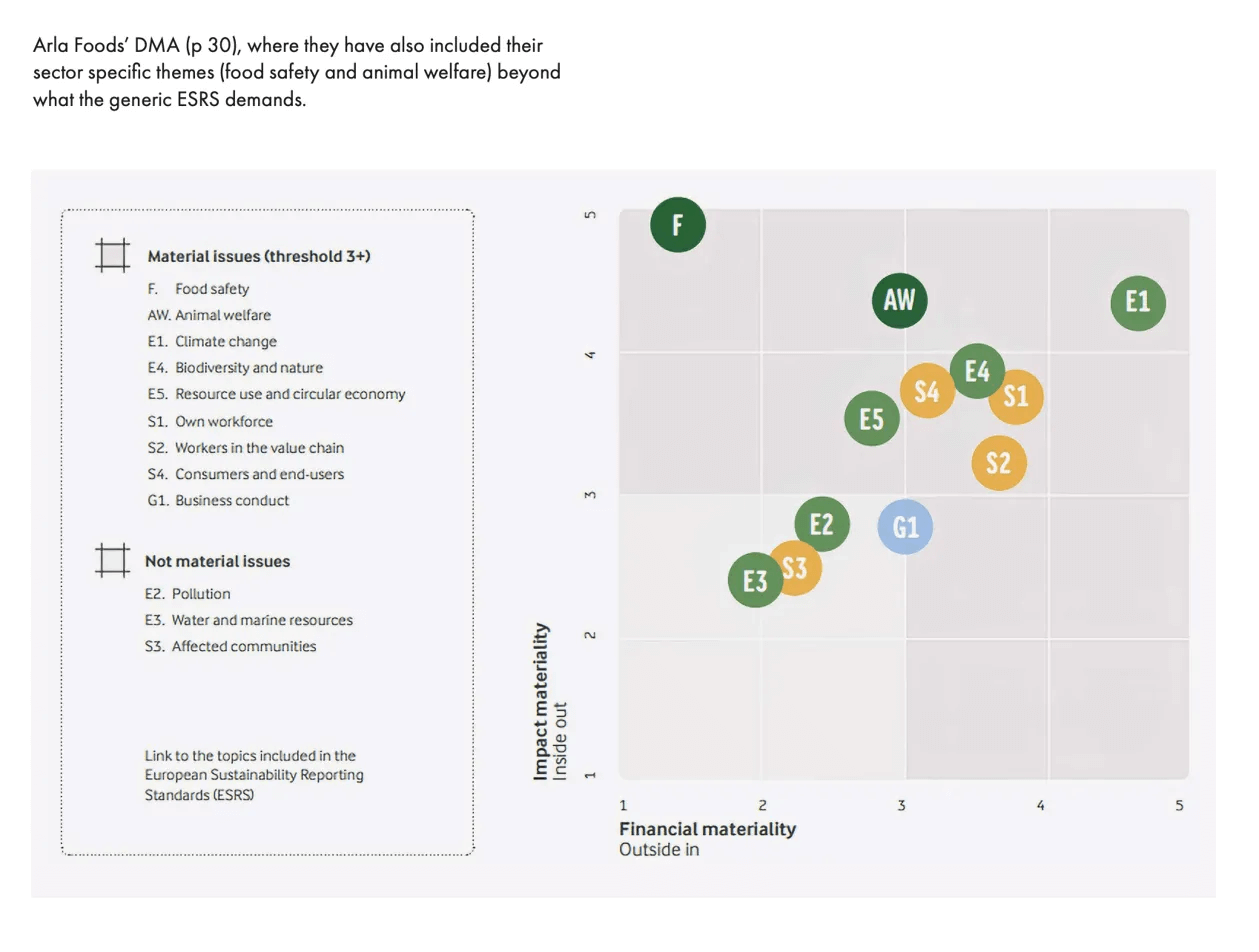

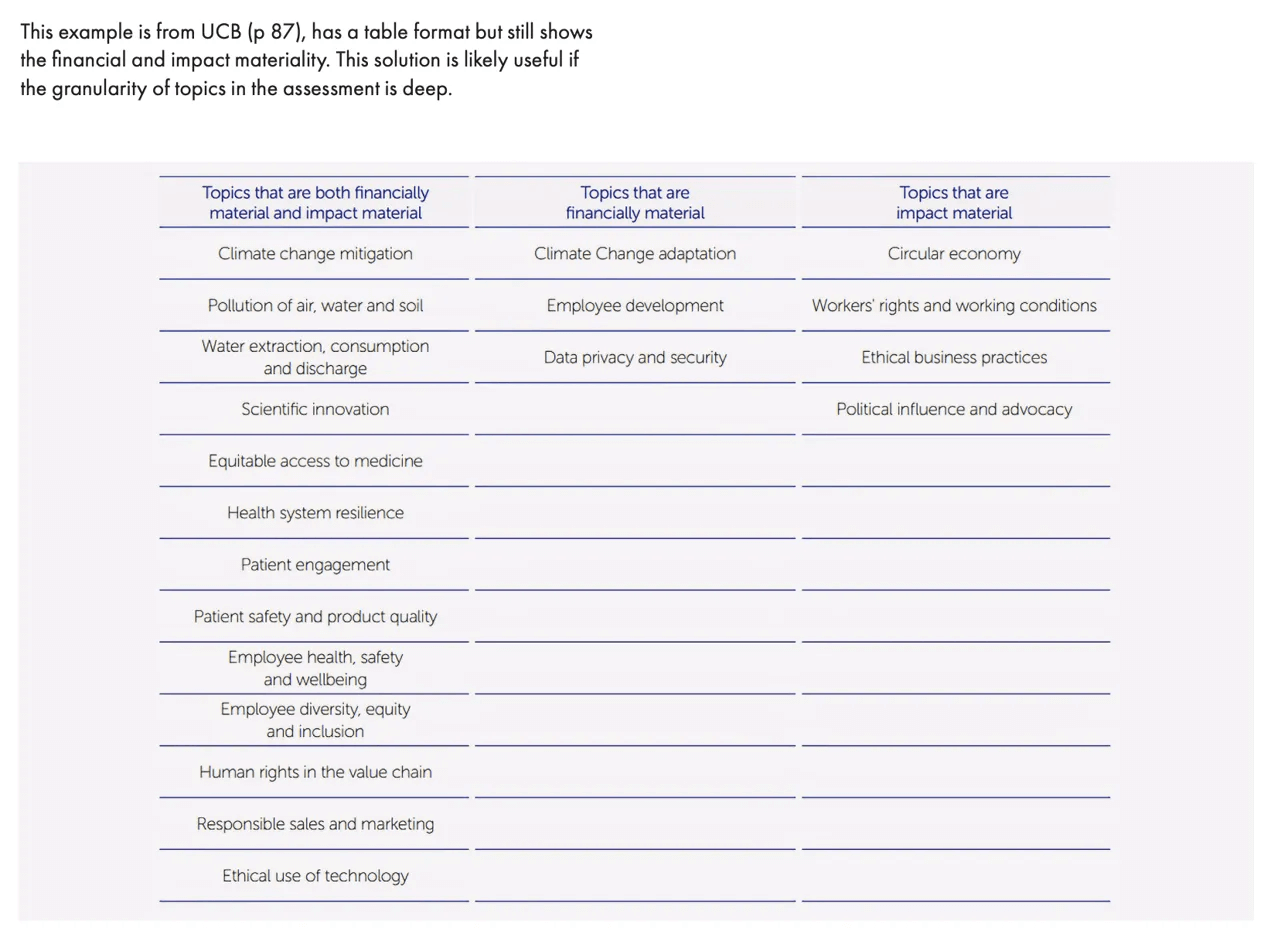

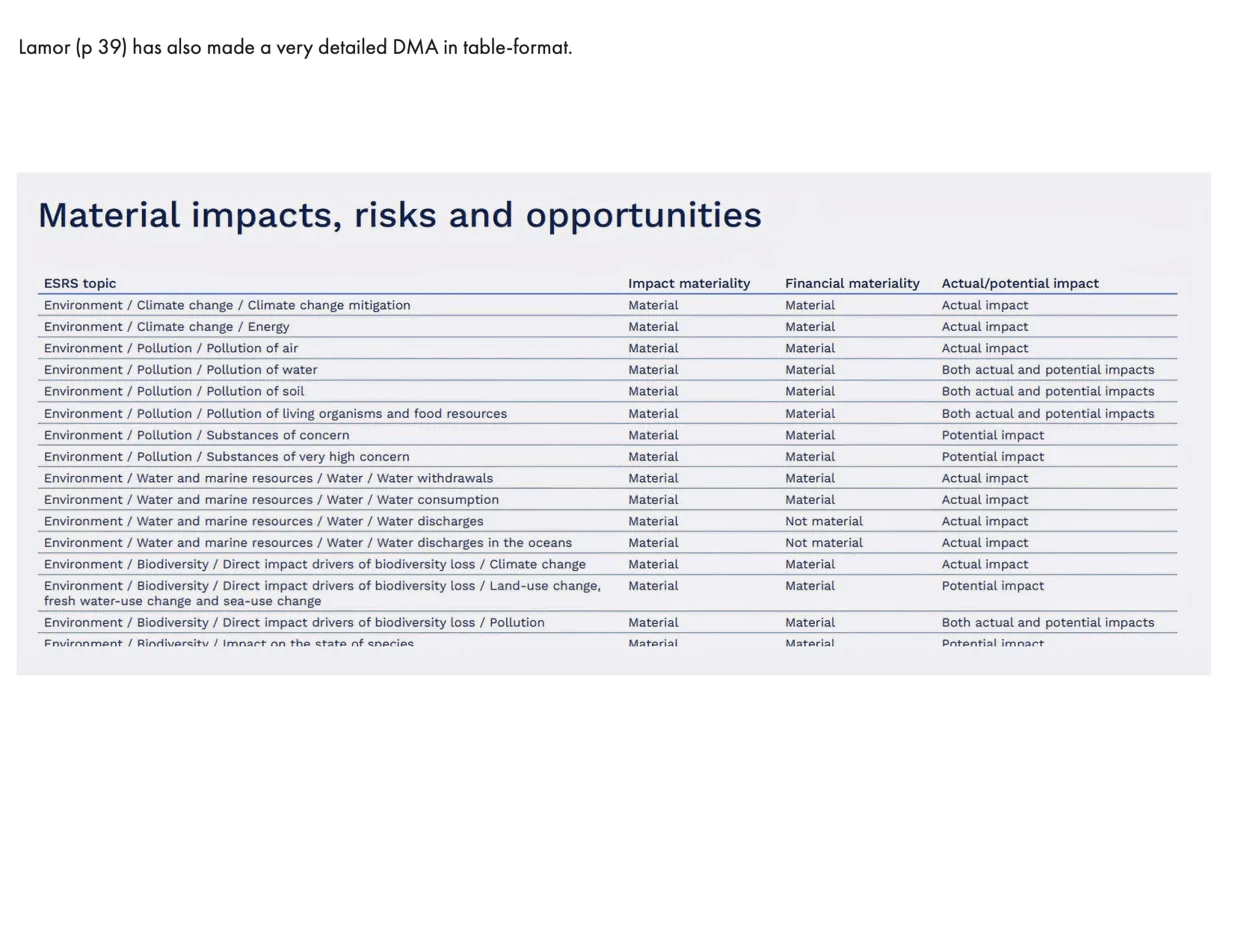

Now, let’s talk presentation. How do you map a 3D reality onto a 2D report? Here are some approaches:

- Classic Matrix: H+H’s approach plots financial vs. impact materiality. Simple, but may oversimplify.

- Sector-Specific Bubbles: Arla Foods adds a third dimension with bubble size. Tailored to industry context.

- Granular Tables: UCB’s method allows for nuanced categorization. Useful for complex topics.

- Detailed Impact Assessment: Lamor breaks down each topic in detail. Great for complex issues, but potentially overwhelming.

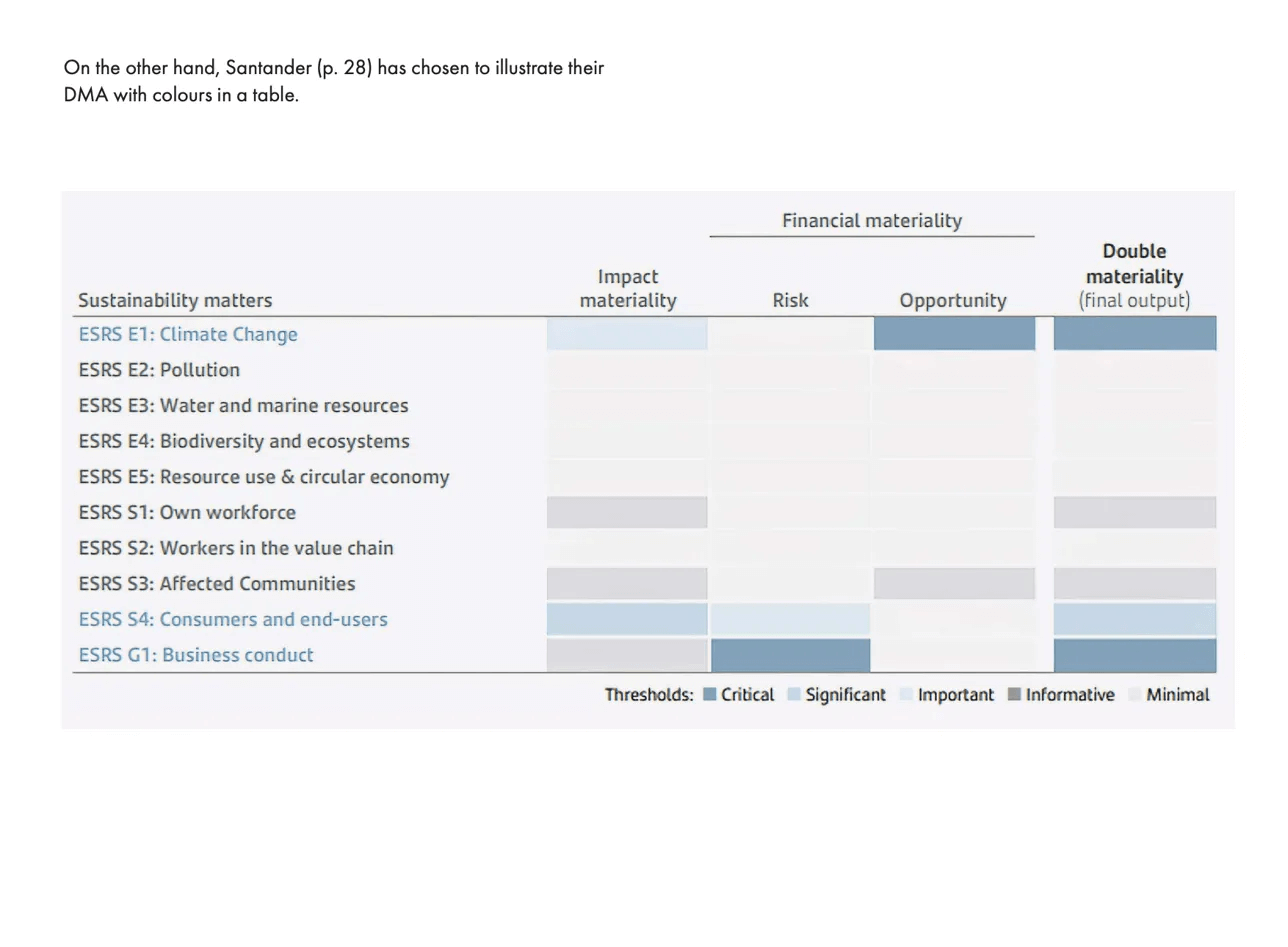

- Color-Coded Thresholds: Santander uses colors to show materiality levels. Allows for quick visual comparison.

Each method has its strengths and weaknesses. The choice depends on the company’s context, complexity of issues, and stakeholder needs. It’s not one-size-fits-all.

Remember, it’s not just about ticking boxes for CSRD compliance. It’s about telling a compelling story of how a company’s financial health is inextricably linked to its impact on the world. It’s a narrative that, if told well, could reshape how we think about business success in the 21st century.

As we move forward, we might ask: How will technology reshape these visualizations? Could AI-driven, real-time materiality assessments be on the horizon? The journey of double materiality reporting is just beginning, and it promises to be as dynamic as the ecosystems it seeks to represent.

Loading...